A Fed pause'll do till a mess gets here

Plus: When are falling rents and used car prices going to show up in inflation data?

“There is no later. This is later.”

The Road

R.I.P. Cormac McCarthy, one of the greatest

June 16, 2023 - Bottom line up top

The Fed declined to hike rates at this week’s meeting but left the door wide open to future hikes should the data require them. While this outcome was a bit more hawkish than expected, markets still doubt that further hikes will be necessary.

With inflation still high on the continent, the European Central Bank could not afford to pause its hiking cycle and instead raised its policy benchmark by 25 basis points, with more hikes expected later this year.

U.S. consumer price inflation continues to slow, with the promise of further deceleration as declining rent growth and used car prices feed through into headline figures.

U.S. producer price inflation has collapsed, with May’s figures coming in even softer than expected. Companies that sell to other companies are feeling their profit margins squeezed as pricing power wanes.

Wall Street equity strategists are hilariously all over the map on whether this new bull market is here to stay or effervescent. Those with recessions baked into their earnings forecasts may need the biggest erasers in the coming months.

Investors, who are understandably unsure where they heck we are in “the cycle” at this point, should consider allocating somewhat more than normal to higher-yielding credit at the expense of equities.

Chart of the Week - China’s “reopening” isn’t going well

The People’s Bank of China cut interest rates this week to help China’s flagging recovery

A July rate hike is a coin toss even after a “hawkish” Fed pause

“They pretend to themselves they are in control of events where perhaps they are not.”

No Country for Old Men

The Fed delivered on expectations this week and declined to raise interest rates beyond the current 5.00 - 5.25% target range. This was the first meeting since January 2022 at which the Fed declined to hike. The surprise, however, came in the updated Summary of Economic Projections (SEP), which showed that only two FOMC members think the central bank’s tightening cycle is over. In fact, a large majority has penciled in at least two more rate increases before the year is out.

A need for tighter monetary policy is fully consistent with the Fed’s new median economic forecasts showing stronger GDP growth, higher core inflation, and lower unemployment compared to the March projections. The Fed’s outlook for 2024 and beyond is largely unchanged and reflects a soft-ish landing for the U.S. economy with rates easing down but still above normal through the middle of the decade.

Financial markets did not take kindly to the new hawkish forecasts until they realized they didn’t believe them. Remarkably, despite the hawkish “dot plot”, investors are no more convinced as of this writing that the Fed will hike in July than they were at 1:59 EST on Wednesday just before the meeting ended. The Fed did succeed, however, in modestly raising expectations for where policy rates would be at the start of next year, effectively dismissing the possibility of rate cuts before year end:

The initial pop in short-term interest rates and swoon in equity markets on Wednesday afternoon had fully reversed within 24 hours. Powell himself may have helped encourage the markets in this direction. Despite a verbal slip in which he referred to this week’s pause as a “skip”, he studiously avoided making a July hike seem like a done deal, and markets followed his lead.

I came into this week thinking the Fed would not have to hike again this year, and I still think on balance that’s the most likely outcome. However, with more than half of the FOMC comfortable hiking at least twice more (or at least saying they’re comfortable hiking twice more), the Fed may need to see soft June employment and/or inflation data to stay patient. If you believe the futures markets, a July rate hike something of a coin toss. But while higher interest rates from here wouldn’t be ideal (and are likely not necessary), investors should prefer another Fed hike or two to a scenario in which the Fed has to begin cutting rates soon because of a significant weakening of economic conditions. After all…

Lost in the minutia of the Fed statement and forecasts is an important question: Why is the Fed even thinking about raising interest rates again? Well, the consensus outlook for the U.S. economy has improved of late thanks to upside surprises like yesterday’s May retail sales and manufacturing reports. The Fed, along with many Wall Street economists, has quietly erased a recession from its forecast as manufacturing activity and home construction recover and consumers remain solid. At the same time, gradual disinflation is well underway with additional downward drivers about to kick in. But for more on that, we need a new section.

U.S. inflation is receding and will fall further this summer

“Your heart’s desire is to be told some mystery. The mystery is that there is no mystery.”

Blood Meridien

May U.S. consumer price inflation data showed continued slowing in food and energy categories, which consumers have already seen for themselves in the supermarket and at the gas pump. But it also showed that prices continue to increase in the heavily weighted shelter category as well as volatile line items like used cars and trucks. The pattern has been the same for three months, now.

Let’s start with food and energy, which helped slow the headline inflation print for May to 0.1% and the year-on-year rise to just 4.0%. This is less than half of the inflation rate in the previous twelve months, making the past year one of the most rapid disinflationary periods in U.S. history.

{kind=link}

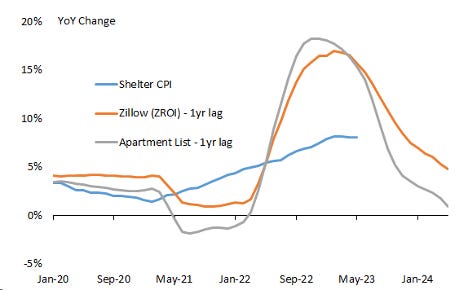

On the other hand, core inflation continues to run well ahead of the Fed’s preferred pace, notching a 0.4% gain in May to match its April increase. The story here has not changed. Shelter dominates the consumer price index, accounting for over one third of its makeup. The largest chunk of that is — bewilderingly — a fictitious price called owners’ equivalent rent, while the rest is mostly rents of primary residences. We know that new lease prices were falling outright by the end of 2022, and while they’ve stabilized in 2023, their annual pace of increase is set to fall below what would have been considered a normal pre-pandemic pace. That’s why we can be reasonably confident that once the rapid disinflation in new leases works its way into the calculation of average leases this summer, the CPI for shelter will switch from a driver of inflation to a drag:

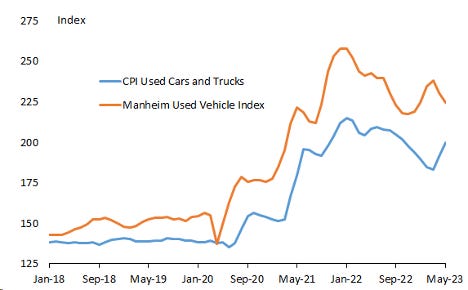

The same is true of used car and truck prices, which have been on a wild ride since 2020. Similar to rent inflation, we can use private sector data to make educated guesses about where the official statistics will go. Monthly used vehicle auction prices usually lead official CPI by a few months and have fallen sharply this spring. If history and logic are any guides, the contribution from used vehicles to CPI should also reverse this summer:

To sum up: Headline inflation is falling just about as fast as anyone could have imagined a year ago (especially absent a recession!), but core inflation — which the Fed rightly uses as a gauge of where policy should go — remains high. Yet we have good reason to believe that it, too, will fall in the coming months. The June CPI report, to be released in mid-July, is going to show another big drop in headline inflation and probably core as well. Just how big a drop will determine whether the hawks get their hike next month or the doves win out and keep rates on hold.

What to watch for over the next week (and beyond)

“Between the wish and the thing the world lies waiting.”

All the Pretty Horses

Nothing gets the optimists’ blood going these days like U.S. housing data. Despite high mortgage rates, chronic underbuilding has led to an acute undersupply of homes. We should see more evidence that builders are set to ramp up construction of single-family homes even as they continue to churn out a record level of multi-family structures.

U.K. consumer prices leapt 1.2% in April thanks in large part to skyrocketing food prices. The Bank of England would love to see that reverse in May’s reading, but with core inflation heading in the wrong direction (up) more rate hikes seem inevitable both next week and beyond.

What the heck has driven stocks up recently? And will it continue? And most importantly, are there better options out there for investors at this point than owning large-cap U.S. index funds? I’ll write about all of this next week.

What else I learned last week

I learned that while I continue to be against punitive tariffs on imports from Mexico, last night’s performance (from the men’s soccer team and its fans) shook my conviction just a bit.

I also learned that the USMNT has to punish Canada on Sunday night for sending all their wildfire smoke down here last week.

I learned that with spring kids’ sports wrapped up, my mind has quickly gone from a sense of relief at not standing on fields all day every Saturday to panic at how to occupy my boys on the weekends all summer.

I learned that a Korean hot pot restaurant should in theory be a stressful meal out for parents with three kids under 11, but somehow with everyone getting their own soup and food to flavor it, it all works. And no one got burned…much.

I learned that the 8-year old kept us all guessing until the last minute about how he’d do as the male lead in his play, but like his dad he’s mastered the art of setting expectations low and exceeding them (most of the time).

I learned that “chalk the walk”, an event in which 2nd graders come outside of their school and draw a chalk mural of their choice on the sidewalk, should always be done during thunderstorms from now on.

I learned that Deadwood is a show that is very deserving of a rewatch if like me you’re finding yourself in a T.V. desert at the moment. Listen to the thunder.

Cheers,

Brian