For investors seeking value, the name's Bond

Plus: U.S. housing market data continues to greatly exceed expectations

June 23, 2023 - Bottom line up top

Global central banks are still hiking interest rates, as most developed economies are experiencing more severe inflation than we currently have in the U.S. The Bank of England surprised with a 50 basis point hike this week and is apparently on its way to over 6% by year end.

Without much new data to go on, investors focused on the global rate hikes and fresh comments from FOMC members after last week’s Fed meeting. Chair Powell’s testimony this week seemed to indicate that the default option for next month’s meeting is a 25 basis point increase, but a lot can change in a month.

Interest rates are struggling to find direction, but Treasury market volatility remains subdued. Inverted bond curves show investors are becoming more concerned about the macroeconomic impact of further monetary tightening.

The U.S. housing market is neck and neck with U.S. consumers for the title of “most surprisingly resilient economic sector” with record multi-family units being built and single-family home construction set to boom over the summer.

For the first time in a long time, bonds are cheaper than stocks. Investors who have held a semi-permanent overweight to stocks (and profited from doing so) should consider rebalancing.

Chart of the Week - The U.K. still has an inflation problem

Core consumer prices continue to accelerate in the U.K., inviting more rate hikes

Investors can “buy low” right now on bonds (vs. stocks)

Wall Street equity strategists appear uncommonly unnerved by the 2023 stock market rally, which few of them saw coming. I expected U.S. stocks to struggle their way to single-digit returns as declining profit margins led to flattish earnings growth while the U.S. avoided recession, and that put me on the optimistic end of the spectrum!

What’s gone wrong with the pessimistic calls? First, the economy has performed better than even my bullish forecast, which has allowed earnings to beat expectations, margins to stabilize, and analysts cease their downward revisions in most sectors. Second, even with economic growth faster than expected, inflation has come down significantly, taking the Fed off the table as a major source of further risk. Third, tech has gone from the 2022 laggard to the 2023 leader thanks to optimism in the sector, specifically around artificial intelligence. The U.S. market has outperformed almost entirely because of its mega-cap technology firms, which are in short supply in the rest of the world.

All of this good news has pushed up valuations on major equity indexes, because investors rightly a) expect earnings to be stronger; and b) see fewer macro downside risks. As those valuations have risen, so have interest rates on inflation-linked U.S. Treasuries, known as TIPS. The gap between the S&P 500 earnings yield (earnings-to-price ratio) and the 10-year TIPS is known as the equity risk premium (ERP), the extra return investors can expect to get by owning stocks over bonds over a period of five to ten years or so. (The reason we compare equity earnings yields to TIPS is that both are real yields, meaning they do not incorporate inflation expectations.) In the last few months, with rates increasing and stocks rallying, the equity risk premium has fallen to its lowest level since 2004:

I’ve been covering asset allocation and markets for over 15 years and until now I’ve never been able to write this sentence: Bonds are more attractive than stocks.

Now, this doesn’t mean the investing in a diversified bond portfolio (let alone the U.S. Treasury market) will deliver better returns than owning the S&P 500 will over any particular time horizon, especially because valuation tells you nothing about expected returns in the short run. It also doesn’t mean a bond portfolio will deliver the kinds of returns investors were used to before 2008, because a lot of the ERP drop has been due to stocks becoming less attractive, not bonds suddenly offering historically-attractively yields. In fact, real yields are still well below their pre-2008 averages. But a low ERP does mean that equity market returns may not compensate investors for their higher volatility to nearly the same degree that they have over the past ten years.

Of course, there isn’t just one bond (or even just one bond market) to fit every investor’s portfolio. Next week I’ll present a deeper dive on what optimal bond portfolio construction could look like, with corporate bonds, in particular, offering a mix of credit and interest rate risk that adds up to a respectable risk-return tradeoff.

U.S. homebuilders don’t seem to think a recession is coming

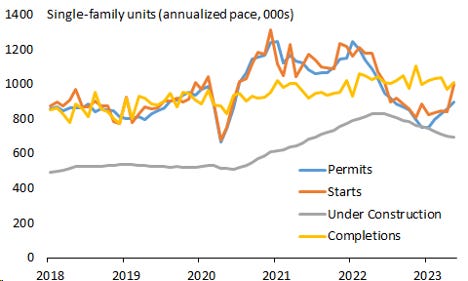

The U.S. residential construction industry has gone from recession to tentative recovery to robust-bordering-on-explosive growth in just six months. The number of multi-family units under construction continues to make new record highs (the grey line on the first graph below) and both permits and starts for single-family homes are surging. Higher growth in multi-family construction is an ongoing response to high rent inflation in 2021 and 2022, which is now easing back down. Permits appear to have peaked almost a year ago, and starts may be peaking now:

Single-family home construction growth has been too slow for over a decade. Starts and permits hit troughs late last year with mortgage rates hitting their highest levels since before the financial crisis. Buyers, however, seem to have shrugged off that constraint, pushing prices higher in most areas of the country and giving the green light to builders to hire more workers and start more projects:

A lot of economists came into 2023 expecting a U.S. recession, but it would be very unusual to see this type of activity in an economy that’s about to contract. The Atlanta Fed’s GDPNow tracker for Q2 shows a positive contribution from residential investment, something that up until recently even the most optimistic forecasters (myself included) would not have expected until Q3 at the earliest. The last time home construction was a tailwind for GDP was the first quarter of 2021.

Demand for housing, especially single-family homes, has simply not been affected by higher interest rates to nearly the degree that economic models predicted. Households are still sitting on excess savings from the pandemic and stimulus, and the supply of new homes over the previous decade has been woefully inadequate to meet the secular rise in demand. That has greatly limited the length and severity of the widely-expected housing recession, which is now clearly over.

We’re still about five weeks away from the Q2 GDP release, but it’s clear that the drivers of economic growth have broadened this spring to include a turnaround in home construction and renewed investment in technology. Resilient consumer demand, including for goods, will also likely stir firms to produce more and restock their inventories, which may not boost sales until later in the year but will add to GDP this quarter.

What to watch for over the next week (and beyond)

Thursday’s Q1 GDP revisions will be old news, but Friday’s May personal income and spending report will likely show another nice gain in real wages but a further slowing in real consumer spending from the past 12 months’ 2.3% pace.

The PCE price inflation metric will reinforce May’s CPI inflation trend: abrupt slowing in headline inflation but stubborn core. PCE core inflation does not have as large a weight toward housing and has stayed relatively contained at 4.7% over the past year. As rents disinflation feeds through further, this number should fall well below 4% by year end.

Preliminary inflation for June in the eurozone should show the YoY rate coming down as the energy shock rolls out, but core inflation remaining sticky. This will invite the ECB to continue hiking, though perhaps not on as brisk a pace as its BoE colleagues.

Consumer confidence readings (we get two next week) are always safe to ignore, but April home price data may clue us into why homebuilders were accelerating their construction schedules in May.

What else I learned last week

I learned that this newsletter becomes less verbose as the school days get shorter. But I promise it won’t disappear entirely — yet — just because the school year is over!

I learned that when you card a 10 on the first hole of an unfamiliar golf course (hitting two trees didn’t help) it tends to hurt your final 9-hole score.

I learned from the exodus of Chelsea players who helped win the Champions League all the way back in 2021 that my 8-year old with a few months of experience on FIFA 2023 could have run the team better over the past year.

I learned that my wife thinks we’re still a year away from “let all three kids run around at the town pool and don’t worry about where they are” mode, but I think we’re already there! Time to catching up on some summer reading!

I learned that after ten long days, summer dance season has started. Thanks goodness, because I think in another week I would have had to replace my floors from all the “at home” tap dancing.

Cheers,

Brian