If you can't stand the heat, stay out of the market

Plus: Diversified portfolios are almost "back" after the swoon in early 2022

“When you can’t make them see the light, make them feel the heat.”

Ronald Reagan

July 7, 2023 - Bottom line up top

This week brought a plethora (Si! A plethora!) of U.S. employment data, virtually all of it showing unexpected strength. Fewer workers are filing for unemployment assistance, hires remain far more common than layoffs, and job openings remain abundant despite their steady decline over the past 12-18 months.

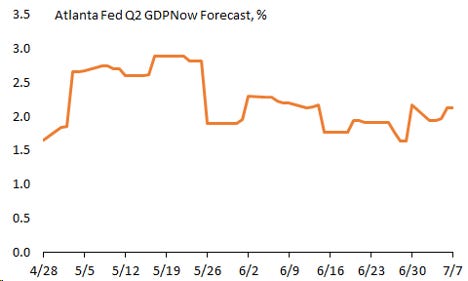

Consumers continue to make big purchases. June auto sales exceeded expectations and will provide a meaningful pop to consumption in this month’s Q2 GDP even after their massive Q1 contribution.

As markets price out recession risks, they are also pricing out much of a chance that interest rates will come down anytime soon. Fed funds futures contracts as far out as May 2024 still have the target rate above 5%. They finally have it right.

Digesting good news was easy for markets in the second quarter as the Fed eased up on rate hikes and inflation seemed to be on its way down. This week’s labor market strength (and the resulting rise in interest rates) was greeted less cheerfully.

The first half of 2023 was marked by softer-than-expected inflation and stronger-than-expected growth, allowing rates to stay relatively steady while risk assets took a chance to retake some of their losses from last year.

Chart of the Week - Dude, where’s my recession?

Economic data continues to show a solid, multi-pronged expansion

The U.S. labor market is not as hot as it used to be…but it’s still hot

I don’t wanna say the U.S. labor market has been out in the sun too long, but this is what the data this week has looked like:

Let’s start with the main event, this morning’s BLS report for June. This report will vex investors and the Fed alike, because it shows a somewhat softer pace of hiring (including some downward revisions to the past few months) coupled with a lower unemployment rate. The unemployment rate is back down to 3.6% because the number of employed workers increased and the number of unemployed workers decreased. This suggests that last month’s concerning divergence from the payroll data was a blip.

Want some more good news? The working age employment rate has risen to 80.9%, the highest it’s been since 2001:

This influx of new workers should help relieve some pressure in the labor market as demand and supply move into some semblance of balance. Wage growth was higher than expected in June but continues to decelerate on an annual basis. Even so, at 4.4% it remains well above its pre-pandemic average.

Ironically, over the past several weeks the scuttlebutt about the jobs market has been that statistical quirks may be causing the Labor Department to overestimate monthly payroll gains. But that theory took a hit yesterday when the ADP, a private firm that produces its own private monthly employment estimate, reported net gains of nearly half a million for June. The lesson, as always, is to consult multiple sources and not put too much weight on a single month of data from one survey. The two BLS surveys and the ADP one all show a cumulative increase in employment year to date of 1.5-1.7 million.

But the list of good news on the employment front doesn’t end there. Initial jobless claims have settled back into their recent range of around 225K - 250K per week after briefly spiking higher in early June. Continuing claims have fallen by nearly 150K from their peak and are now back to their lowest level since February. This low rate of layoffs is corroborated by the May JOLTS report, which showed involuntary discharges remain uncommonly uncommon. This data is noisy and unreliable month to month, but it paints a pretty clear picture if we zoom out: workers are still quitting their jobs slightly more often than they were pre-pandemic, job openings seem to still be very high (assuming we’re measuring them correctly), and the rate of hiring greatly exceeds the rate of firing.

To sum up, the U.S. labor market is cooling very gradually from a very hot starting temperature. On balance, while the pace of hiring has slowed, other indicators still show demand for labor continuing to exceed supply, which could mean persistently high wage and price inflation. Markets correctly interpreted the totality of this week’s data as suggesting the need for higher interest rates for longer.

How did things go so right for investors in the first half of 2023?

Is it really as simple as “what goes down must eventually come back up”? After a terrible nine months to start 2022, financial markets have rallied back strongly in the last three quarters:

As a result, a 60/40 portfolio of U.S. stocks and bonds is within striking distance of its peak from the end of 2021:

U.S. equity markets performed especially well in the second quarter, reversing some of their recent underperformance. An end to U.S. dollar weakening, significant underperformance in all things China, and an outsized rally in technology stocks all played a part.

The second quarter was also notable for what did not occur. Coming into April, there were understandable widespread fears of contagion in the banking system after the failure of SVB and several other regional banks. But neither a banking crisis nor the broader recession that many economists have been expecting materialized. In fact, economic data — in the U.S., at least — has been surprising on the upside while inflation has been coming in slightly softer than forecast:

This week’s news on the labor market — along with a “hot” ISM Services business opinion poll that is worth ignoring even if it confirms your priors — resurrected the “good news is bad news” mantra that the media loves to repeat. But zooming out from the last few rough days, good economic news has propelled a lot of this year’s risk-on rally. However, too much economic heat could prevent stocks from returning quickly to their January 2022 highs. That’s because on the other side of the stronger growth coin lies higher inflation and interest rates. And we know from last year’s experience what those can do to investors’ risk appetite in extreme cases.

If you had told me back in March that the Fed would still be talking about hiking rates multiple times in the second half of the year but the S&P 500 would still be up 7.5% with 2023-24 earnings estimates little changed, I would have been surprised. All of the move has come from valuations. Stocks spent Q2 getting pricier 1) without interest rates establishing a clear top; and b) with recession still the consensus view. In other words, stocks have priced in a Goldilocks/soft-landing scenario. To be clear, I’m sympathetic to this view, which is one reason I currently prefer bonds, which have not rallied and continue to offer more attractive risk-adjusted returns, to stocks.

Looking forward, I continue to hold the view that a durable rally in U.S. stocks back to their all-time highs will require either unexpectedly good earnings data over the next few quarters or a clear sign from the Federal Reserve that inflation is licked and rates will soon come back down in a gentle fashion. With the latter looking less likely for at least another year, we’ll need to see more upside economic and earnings surprises to give stocks the support to move higher.

What to watch for over the next week (and beyond)

June U.S. consumer price inflation data will arrive on Wednesday and should show another large decline in YoY inflation. Headline CPI has likely only risen a little over 3% in the last twelve months, but core inflation will come in closer to 5% with shelter costs leading the way.

Lots of discussion lately about the lagged effects of tighter monetary policy, but the signaling effects of prospective rate hikes have arguably been more powerful in this cycle. With the promise of many more rate hikes coming in the U.K., we’ll see if monthly growth or employment data is showing the effects just yet.

What else I learned last week

I learned that I did not go to the White House last week and I certainly didn’t leave anything there.

I learned that throwing hundreds of water balloons at passing local firefighters firing them back from on top of their engines has become a cherished family tradition in my household. America, baby!

I learned that Miami is still as hot as I remember it, but also pretty empty after July 4th. Things are so dead here that I almost got into a night club. Almost.

I learned that when the fire alarm in your hotel goes off at 3:45am and you file down to the lobby only to find that only one other guest has bothered to do the same, it makes you question a lot of things.

I learned that Indiana Jones remains a great 1980s trilogy…and that’s all.

I learned after a 2 hour, 40 minute trip to go 66 miles from my house on Long Island to a family party near Red Bank, New Jersey, that the Staten Island Expressway needs to be prominently featured in Dante’s Divine Comedy, Part 2.

Cheers,

Brian