The Fed has questions. Investors need answers.

Plus: Private sector balance sheets still look really strong. Film at 11.

“The right word may be effective, but no word was ever as effective as a rightly timed pause.”

Mark Twain

June 9, 2023 - Bottom line up top

Investors had a chance to take a breath this week after a series of scares from the banking failures and debt ceiling drama. But the cloudy macro outlook provides few clear signals for stocks or bonds.

The risks of a U.S. recession this year, which were never as high as advertised, fell further this week as more data confirmed private sector balance sheets remain in good shape.

The Fed will not hike rates next week. Whether that is interpreted as a “pause” or a “skip” will depend on the central bank’s updated economic and interest rate projections as well as the public statement from Chairman Powell.

Developed economies in Europe, where consumers have been battered worse by negative real wage growth and declining savings over the past year, are flirting with recession if they’re not already in one.

U.S. stocks have entered a bull market in the midst of declining volatility and a solid economic backdrop. But with valuations already stretched, new catalysts will be required for the S&P to regain its all-time high anytime soon.

Chart of the Week - Global goods are flowing like wine

{kind=link}

The Fed’s Global Supply Chain Pressure Index has plunged to an all-time “easy” low

The “everything is terrible, but I’m fine” economy endures

It’s been almost a year since Derek Thompson’s article for the Atlantic attempted to explain the economic doomer-ism adopted by a large slice of U.S. consumers and businesses even as most of them see their own financial situations as solid. Since mid-2020, the U.S. economy has staged its strongest economic comeback in decades, but relatively few people seem to recognize it. A few weeks ago, I wrote about the University of Michigan Consumer Sentiment survey’s inability to serve as a predictive — or even a concurrent — gauge of consumer behavior. And last week, I pointed out that the ISM Manufacturing poll hasn’t mapped onto real manufacturing activity in several years. Opinion polls simply don’t match real activity.

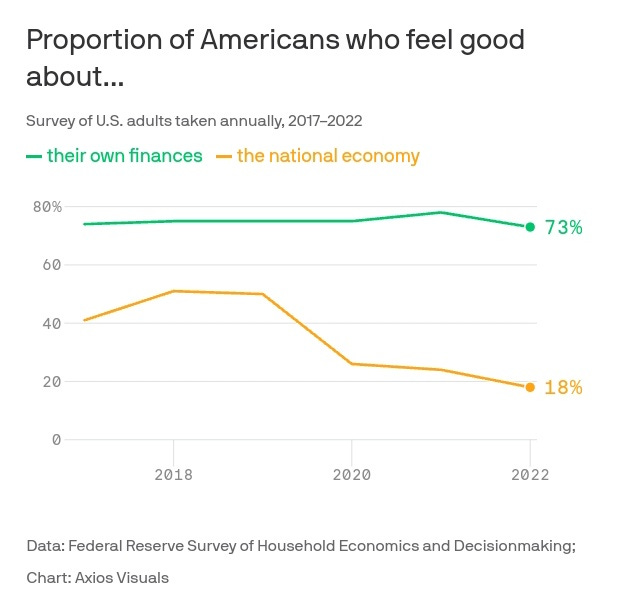

An annual Federal Reserve survey conducted last October, when economic growth was weaker and inflation was higher than today, shows the percentage of people who felt good about the national economy was lower than in either 2020(!) or 2021 even as most felt good about their own finances:

My guess is the 2023 survey won’t look much different despite the impressive job creation and rapid disinflation. Nothing in the recent sentiment polls makes me think the yellow line will revert to anywhere near its 50% pre-pandemic level. Fortunately, the green line is by far the more important of the two, and nothing in employment or consumption data indicates widespread concern among households. Also, as I never miss a chance to point out, incomes have been rising faster than prices for almost a year.

Speaking of incomes, this week gave us a stable but comprehensive look under the hood of household balance sheets and cash flows. The Fed’s Q1 National Accounts data showed household net worth climbed by an impressive $3 trillion thanks to rising equity markets and only a slight decline in home values. At $149 trillion, total net worth is still down from its $153 trillion peak in early 2022, but it remains 27% above its Q4 2019 level. One detail in the report that may be of some interest is the large increase in holdings of money market mutual funds and debt securities, at the expense of bank deposits, as of March 31st compared to the end of last year. This was both a cause and an effect of the multiple regional banks failures earlier this spring. A second point to note is that debt for both households and non-financial businesses fell as a share of GDP. We’ll get data on debt service costs and financial obligations, which take into account not just the size of debt but the cost of servicing it relative to disposable income, in a few weeks. I know you’re as excited as I am.

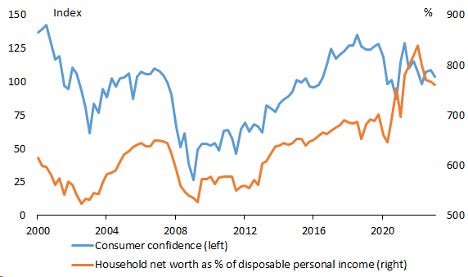

As a share of disposable personal income (which also rose sharply in the first quarter) household net worth has been correlated with consumer confidence over time. But like so many others, that relationship has broken down since 2020:

Analyzing a piece of data that arrives only quarterly — and on a considerable lag, to boot — can be frustrating, but there’s a reason I do it. The massive hit to household finances in 2008 set the U.S. economy up for an unusually sluggish recovery. But while asset prices did not fully recover from the Great Recession until the mid-2010s, they recovered from the onset of Covid-19 in a matter of weeks. This V-shaped market recovery, along with the considerable fiscal and monetary aid that enabled it, created enduringly confident consumers (despite what they say) and a stronger base for economic growth even years later.

Fed preview: A pause? A hold? A skip? A tap dance?

Is the Fed done hiking rates? Last month, in my inaugural Substack newsletter on May 5th, I said it was. And I still think so. But the market disagrees. In fact, there’s been a significant sea change in the pricing for future Fed hikes since early May:

The rate hikes priced in for the second half of this year are largely gone, and the pace of expected cuts into 2024 has slowed. But now there’s a kink in the short end of the fed funds futures curve, with a rate hike priced in for July and the balance of risks only turning to cuts in November.

While the “hike in July, cut by November” scenario would be pretty wild, it’s also pretty unlikely. Reading between the lines of recent FOMC leadership statements, the better bet is that the Fed will make no further change to interest rate policy this year in either direction. Many members still want at least one more hike, as the median “dot” in the updated Summary of Economic Projections (SEP) next week may show. But these hawks are running out of time, with auto and shelter disinflation set to pull inflation down over the summer and remove the urgency to tighten. Annual consumer price inflation should be below 3.5% by the time the FOMC meets again. So while it’s reasonable to argue for a hike at next week’s meeting (we could see a hawkish dissent or two on a pause), it will be harder to justify one in July, let alone September. All the doves need to do is hold onto the ball and run out the clock.

Questions that need answering

The next major monetary policy questions center on getting things back to normal in 2024. What does the Fed think the neutral interest rate is? When will it be time to cut? How large and frequent will those cuts be? Fed Chair Powell’s press conference will be focused on inflation vigilance as he leaves open the potential for more rate hikes to stop financial markets from loosening prematurely. But at least one reporter will ask him whether the committee discussed the plan for getting rates back down to neutral. Only if and when the Fed begins cutting will we know whether the economic “landing” is hard or soft. And that may not be until well into 2024.

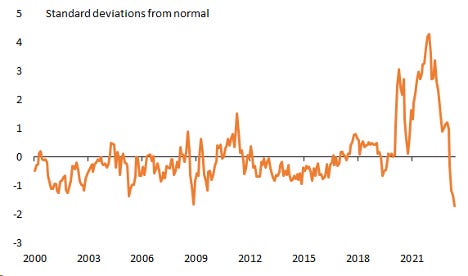

One last point about the tightening: Financial conditions have eased considerably from the moment of peak hawkishness from the Fed back in late October:

To be fair, this graph doesn’t tell you the whole story. The effect of the banking scare in March and April was probably more economically important than the relatively brief and mild market reaction would indicate. And the recovery in public equity and credit markets is occurring even as conditions seem likely to worsen in private markets for multi-family housing (where supply has risen rapidly), office real estate (where demand has been very slow to return), or private equity. In other words, we’re not out of the woods on growth, and inflation has not yet moderated enough to let the Fed declare victory. But that date seems to be getting closer.

What to watch for over the next week (and beyond)

I said enough about the Fed above, but the ECB meets, too, and will almost certainly be raising rates by 25 basis points despite the larger-than-expected drops in May inflation prints across the continent. The fun probably stops with another hike this summer as Europe’s economy starts to look a bit shaky.

Falling food prices and stabilizing shelter costs probably helped slow U.S. consumer price inflation last month. May and June will show the largest year-on-year drops in headline CPI thanks to base effects, i.e., the surging energy prices from last spring rolling out of the one-year window. But we may still get another month or two of rent and used cars propping up core prices before they roll over.

Global retail sales growth has been weak for several months, but the U.S. has been the exception and releases its data earlier than most other major economies. I expect weaker growth in May than we saw (unexpectedly) in April but no signs of a collapse as restaurant and online sales seems like to remain firm.

What else I learned last week

I learned that as I walked to pick up my 5-year old at school on Wednesday with a dark orange smoke-stained sky overhead, I half expected to run into a replicant Harrison Ford in a casino. At the very least, I was bummed not to have my holographic Ana de Armas companion with me.1

I learned that Spiderman: Across the Spider-verse was jaw-droppingly (a term you only tend to see in movie reviews) entertaining, kept my two boys (8 and 5) throughout, and delivered an agonizing but well-earned cliffhanger. Bravo!

I learned that other than an 8-year old with tummy troubles having to bow of out attending at (literally) the last minute, the wife/daughter dance recital combo was a splendid and efficient use of my time last weekend.

I learned that our town’s public schools, which I attended myself and love, need to find better ways to occupy the kids in June than “let’s invent yet another reason for your parents to come into school for 20 minutes to watch you do something unremarkable” each and every day.

I learned that revisiting 10 Things I Hate About You with my 10-year old actually caused *her* to scold *us* for showing her something so inappropriate. I’ll admit, it’s a harder PG-13 than I remember. But still a very rewatchable late 90s classic.2

Cheers,

Brian

Blade Runner 2049 is one of the best movies of the 2010s and remains criminally under-appreciated. Thank you for reading this footnote.

“My daughter is not getting jiggy with some guy, I don’t care how dope his ride is.” Words to live by.