What's around the corner for the U.S. economy?

Inflation is coming down, but growth is still quite strong. Is that a problem?

The U.S. economy came out of this week stronger than it went in, but the same cannot be said for my very old laptop. Apologies for the delay as I scramble to put some thoughts together using my brand new MacBook Air. Hopefully it lasts as long as its predecessors did, meaning I won’t need a new one until 2033.

July 28th, 2023 - Bottom line up top

The soft landing narrative that’s taken hold in U.S. financial markets was all but endorsed by the Federal Reserve this week, and a slew of data points showed strong growth and significant disinflation.

U.S. consumers continue to buy stuff, closing out Q2 with a strong burst of real (after inflation) spending. The resilience of goods demand, in particular, should give pause to those of us (like me) who so often referred to consumer behavior in 2021 and 2022 as warped by the pandemic and likely to normalize quickly.

The Fed raised interest rates but didn’t make a big deal out of it. Whether it needs to hike again will depend on whether its reaction function is more sensitive to softening inflation (in which case no need for more hikes) or reaccelerating growth (in which case there could be more but possibly not until 2024).

U.S. GDP grew at a surprisingly strong 2.4% annualized rate in Q2 even without help from rebounding home construction or inventory restocking. Q3 is already shaping up to be another solid-to-strong quarter.

June personal income grew faster than inflation yet again, which seems to be the key to understanding why consumer confidence surveys have begun to turn higher.

Stocks seem to like all of this strong growth, which correlates well with earnings. But bonds are less enthusiastic about the higher-for-longer outlook for policy rates.

The U.S. economy has turned a corner. What lies around it?

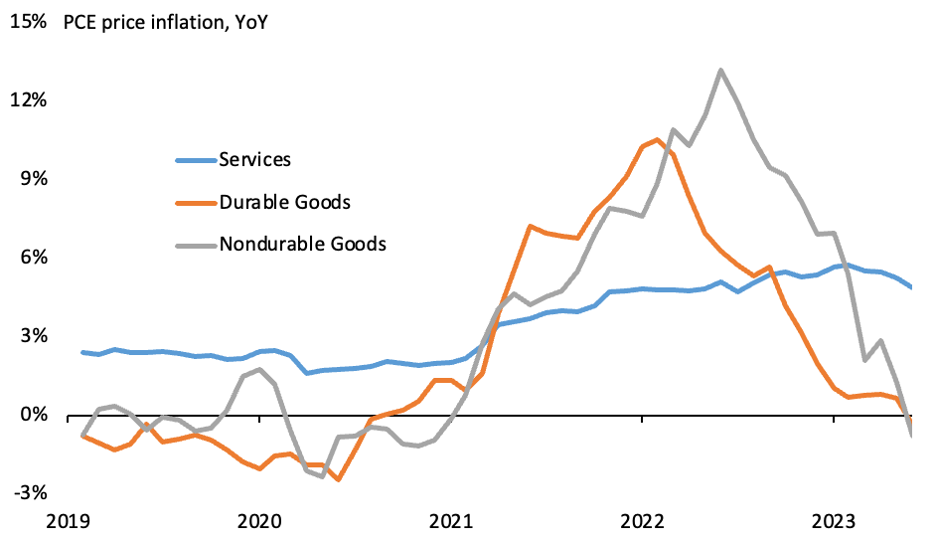

Can inflation fall from 9% to (close to) 2% in a large and diverse economy without a recession? It seems as if we can answer that question in the affirmative after this week. Headline and core PCE inflation both annualized at close to 2% in June, and there is good reason to expect the next few months’ readings to remain soft. Meanwhile, while wage growth has slowed, it remains somewhat above average even as price hikes have become rarer. Few if any economists are still calling for policymakers to engineer a recession in the name of licking inflation. It looks pretty darn licked already:

What’s weird about inflation looking pretty darn licked is that economic growth is still humming. Yes, the relatively stale Q2 GDP report showed strong and broad-based growth, but the big news is that a few of the tailwinds I expected to see in last quarter’s data weren’t there, meaning they are likely to show up in Q3 and Q4. Home construction is rebounding, with permits signaling more in the pipeline. Persistent consumer demand for goods will cause companies to ramp up production and restock their inventories in the second half of this year. And an extra push from a variety of government initiatives passed last year already have some high-profile forecasters, including the bullseye-hitting Atlanta Fed’s GDPNow Index, to forecast a further acceleration in growth in the current quarter.

Bloomberg columnist Conor Sen is a great Twitter (and Threads) follow, and he’s been dead on for the past 6-9 months in predicting the resilient growth/softer inflation scenario just the way it’s played out. He had a great post this morning summing up the four socially acceptable positions to hold on the U.S. economy:

It’s getting harder to be a “1” in the short term with core inflation likely to break down toward 3% in the next two or three months based on what we know will show up in the used cars and shelter figures. A close follower of the Leading Economic Indicator Index could still find a case to call him or herself a “2”, but at this point you’re leaning pretty hard on the weak PMIs and the inverted yield curve. All of the other financial market indicators (i.e., stocks and credit) along with capital goods orders, consumer confidence, unemployment claims and building permits are showing promise. I’ve been a “3” for a long time, but it’s in my nature to worry anytime I find myself in the Goldilocks camp, and right now what I’m most worried about is the “no landing” scenario we’d find ourselves in at number 4.

If you believe the Fed’s estimates and forecasts, policy is currently quite restrictive yet employment continues to surge and growth in many areas of the economy is accelerating. But the obvious conclusion based on what we’re seeing with our own eyes is that policy is not actually very restrictive, meaning that the Fed’s estimate of the neutral target rate, which has been pegged at 2.5% since mid-2019, is too low. And that’s good! Because if 2.5% really was the neutral rate, the Fed’s current 5.375% target rate would likely be taking us into recession.

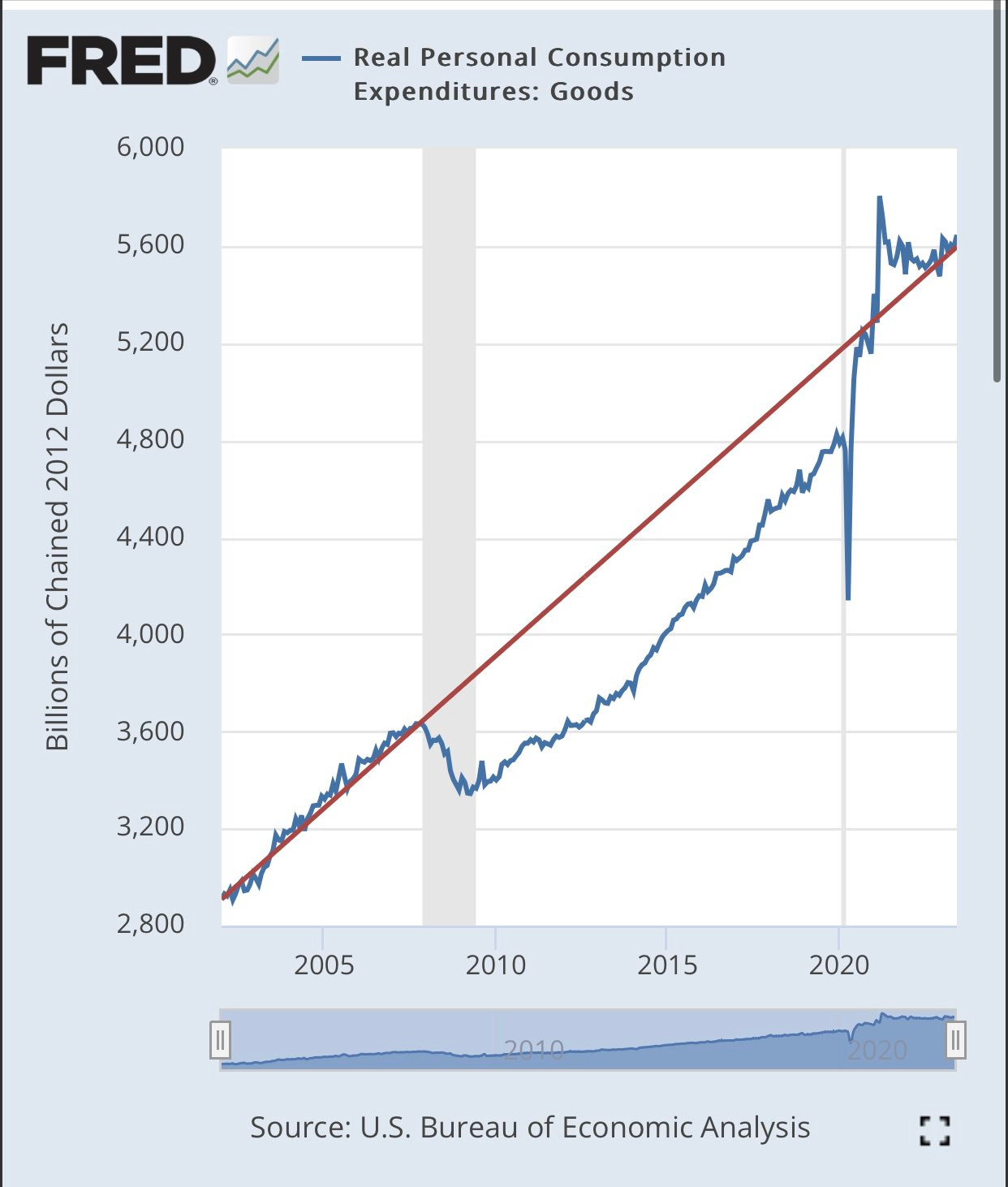

Now, 2.5% felt like a restrictive policy rate for pretty much the entire 2010s and even as recently as 2021. But investors today don’t see any chance that the Fed will get back down to it until well into 2025. And they’re probably right, because the economy seems capable of running at a higher speed with higher interest rates (and maybe higher inflation) than it did in the decade following the financial crisis. Take a look at what real consumer spending on goods has done vs. trend. We’re back to where we would have been if the mid-2000s growth had continued past the crisis:

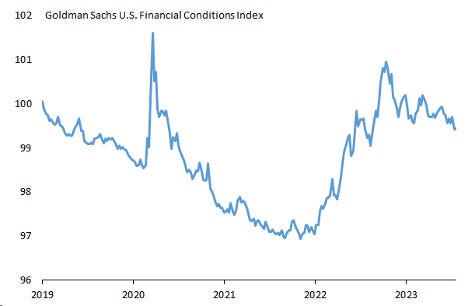

It’s not just consumer demand telling us that higher interest rates are A-OK. The U.S. housing market did not escape 2022 without its share of bruises, but home prices and construction are rebounding even as mortgage rates continue to climb. Growth in U.S. wages and salaries picked up again in May and June. Yikes! And, of course, the strongest case for “policy is actually still pretty accommodative” is that financial markets seem to think so:

This chart has become a Rorschach test for economists. If you’re a “3” see inflation coming back down to target on a smooth path from here, you’re not particularly worried about the fact that markets are so calm right now. If you’re a “4” and think inflation’s dip back to target will be brief (i.e., transitory), you probably think conditions will need to tighten further, which means more action from the Fed and (probably) a return to losses for investors as the risk of contraction in the second half of 2024 rises.

Longtime readers (well, those who have been reading me for at least a year) know I’ve been on the optimistic end of the spectrum when it comes to the U.S. economic outlook through the middle of this decade. I still am. But now the S&P 500 is 27% off higher than its level at the end of Q3 2022, corporate bond spreads are tighter than they’ve been in a year, and the 10-year U.S. Treasury yield is trading in a tight range well below its 52-week high. There’s not much low-hanging fruit left to be plucked in markets, and it seems like more could go wrong than right based on what’s priced in.

What to watch for over the next week (and beyond)

The July U.S. jobs report hits on Friday. The median expectation is for just under 200K new jobs, down a bit from June’s 209K. But any number in the 150K-200K range would be just fine assuming it was accompanied by a stable unemployment rate and gradual deceleration in average hourly earnings.

What else I learned last week

I definitely learned not to leave a running 10-year old laptop in a backpack in the trunk of a car during a bad heat wave.

I learned that when you order breakfast at a French restaurant during a job interview and point to the thing on the menu you think says “egg” and they bring you a single soft boiled egg in a fancy cup like it’s 1925, you just have to eat it in the least embarrassing way possible. It was actually really good.

I learned that the trip down to Philly with my boys was more than worth it to a) see Chelsea win a thriller; b) have my 8-year old’s favorite player, whose jersey he was wearing, score his first ever goal for the club; and c) hear my sons boo the Eagles (who weren’t even playing) in their home stadium and live to tell the tale.

I learned that my 10-year old made it through her week at sleep away camp, apparently coping with homesickness by writing letters to every member of my extended family like she was about to fight in the Battle of Antietam.

I learned that the dirty martinis at Sparks Steakhouse are so good that I can barely recall making a vulgar gesture in the general direction of a certain nearby building. Maybe it didn’t happen at all. Who knows?

Back on schedule next week with a breaking report on the July jobs numbers!

Cheers,

Brian