Goldilocks and the three bear scenarios

Also: Why the best asset class for a U.S. Treasury default could be...U.S. Treasuries?!

“There may be trouble ahead. But while there’s moonlight, and music, and love, and romance, let’s face the music and dance.” - Irving Berlin

May 12, 2023 - Bottom line up top

Despite the vibes, there’s just not much evidence the U.S. economy is heading for a recession. This week’s inflation reports contained mostly good news about waning price pressures, which will keep the Fed on hold for now.

While the labor market has softened slightly, parts of the economy like housing and manufacturing that were in recession over the past year now seem to be cycling up, providing a cushion against any weakening in retail spending.

Risk assets are pricing in something like an economic soft landing while interest rate futures show rapid Fed easing. These two views cannot peacefully coexist, and their eventual conflict presents a risk to markets over the balance of 2023.

Bank loan officers tightened conditions in the first quarter amid the March deposit run, but not at an especially alarming pace. Both loan supply and loan demand are falling. The latter may be the more concerning sign.

Stocks are treading water, caught between a good first quarter earnings season and concerns about credit conditions and a debt ceiling breach. A large leg up from here is still hard to imagine in the near term.

Long-term interest rates peaked months ago, but credit spreads are resisting both the banking scare and concerns about slower economic growth. Yields on various types of credit remain attractive compared to equities.

Chart of the Week

The San Francisco Fed illustrates the stunning trend in excess household savings Read the whole paper!

First quarter U.S. corporate earnings were better than expected (or feared), but reporting season is now largely over. The April U.S. employment report was impressive but has already faded into the rear view mirror. Disinflation in consumer and producer prices is proceeding. And the widely-hope-for Fed interest rate pause in June is fully priced in. So while a Goldilocks-ish soft landing remains my base case, it’s going to be a while before we’ll get much more evidence that it’s playing out that way. On the other hand, if you’re hunting for potentially bad news, you’re entering a target-rich environment. It’s Goldilocks and the three bear scenarios.

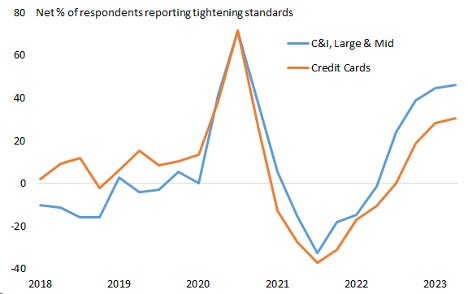

Bear scenario #1: Tightening credit standards and falling loan demand

The U.S. regional banking scare is both a cause of heightened recession fears and an effect of tighter monetary policy. This week’s new piece of data — a survey, yes, but a good one — was the Fed’s Senior Loan Officer Opinion Survey (SLOOS) for April, taken just after SVB and Signature Bank failed and market volatility was near its apex. The SLOOS isn’t normally a market mover, but any knock-on effects from the drop in deposits and asset values at many banks over the past several months could lead to slower growth and poor equity and credit market returns. So what did the survey say?

{kind=link}

Bank lending standards tightened in the first quarter, but not at an alarming rate

Businesses’ demand for loans is in recession territory

Remarkably, banks did not report a significant further pace of tightening in lending standards beyond what they’d reported in the prior quarter. But lending is undoubtedly getting tighter. More concerning, however, is the drop in demand for commercial and industrial loans, i.e., loans to businesses of all sizes, which could mean many have scaled back plans to hire and invest, two things we know contribute to forward-looking growth.

Consumers used credit cards to fuel their strong spending growth in late 2021 through most of 2022 but have been swiping (or inserting…or tapping…or doing whatever Apple Pay is…) less in recent months. This is consistent with the higher real incomes, higher savings rates, and slower consumption growth we saw in the Q1 GDP report.

The primary risk to the economy in this scenario is a further deterioration in bank balance sheets leading to a harder jerk back on credit growth. We didn’t see that in this week’s report, but that doesn’t mean we’re out of the woods.

Bear scenario #2: The debt ceiling mess

The U.S. Treasury is going to hit its borrowing capacity sometime in the next few weeks, which would result in either a U.S. Treasury default or something close to it (e.g., the minting of the platinum coin, payment prioritization, or some other unilateral executive action of dubious constitutionality) unless Congress raises it. It’s very likely that default will be averted, probably at the last possible moment. But when making predictions like this, it’s useful to have data to back it up. In this case, all I have is recent history and a hope that sane heads prevail.

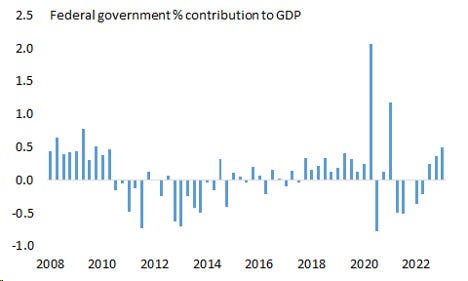

Nevertheless, shortly after the 2022 election, I wrote that divided government — specifically this kind of divided government, with a Democrat in the White House and at least partial Republican control of Congress — posed little legislative risk to markets but was likely to struggle with the basic tasks of government like borrowing money and passing budgets. We last had this arrangement in the early 2010s, a period that produced routine dysfunction and damaging austerity. Right now, austerity (i.e., fiscal tightening) would be less harmful with nominal GDP growth nearly doubling its average during that period. The federal government’s contribution to GDP, while down massively from the stimulus heyday during Covid, has been positive for the past three quarters even as inflation runs hot, advising at least some belt tightening at the federal level (especially with more states running expansive fiscal policies).

The federal government’s contribution to GDP has room for pruning

But here’s the problem: The debate over taxes and spending can wait until the fall, but the debt ceiling needs to be raised well before that. This timing mismatch is unfortunate, and markets have taken notice. The yield on the 1-month Treasury bill is up over 2% since mid-April, as the dead ceiling deadline has moved to within a four week window. That’s credit risk being baked into the most important and most liquid bond market in the world. Not great.

My probability distribution for debt ceiling outcomes looks something like this:

A comprehensive budget solution and debt ceiling raise by June: 0%

A “punting” of the debt ceiling until the fall budget showdown with some small spending cuts or other measures like permitting reform thrown in so it doesn’t look like the Republicans caved: 95%

Into the abyss: 5%

Lest you think this is too optimistic, a 5% chance of a catastrophic outcome is really high! The odds of the Treasury defaulting on any given day are closer to 0.00005%. This is why despite the fact that the two sides are at least talking this week, risk assets are unlikely to stage a durable rally until the coast is clear.

Bear scenario #3: Hawkish monetary policy (relative to expectations)

Consumer price inflation was high again in April. But the list of major contributors to inflation is getting smaller, and wholesale price inflation (what companies pay to other companies) has just about normalized. Gasoline prices rose last month, offsetting falling costs for natural gas and electricity. Used car prices accounted for a large chunk of the monthly increase, but most of inflation is still shelter costs. Because CPI uses average rents, it’s been slow to respond to the drop in new rents over the past nine months. That rent inflation has peaked will become clear in the reports over the next few months.

Consumers are also finding that prices for food (at least if you’re not buying your food in restaurants) and new cars have stabilized while those of large durable goods like appliances and furniture are still falling. Most importantly, the components of the consumer price index that are sensitive to labor costs are rising more slowly than they were a few months ago. The Fed’s “supercore” measure, Core Services ex Shelter, barely rose at all in April, helping bring down its year-on-year increase to 5.1% from a peak of 6.5% last September:

If you worry about inflation because it can hurt real consumer spending, this report should make you feel better. Most households are not buying used cars, and the shelter cost calculations in CPI are either fictitious (owners equivalent rent) or starting to trend down (rent of primary residence). Most U.S. households are seeing strong real income growth and have ample savings with inflation receding.

But if you worry about inflation because it may compel more hawkish monetary policy, you may still be losing some sleep after this report. True, the Fed will view the drop in supercore inflation as reason enough to stop hiking for now, but that outcome was already priced in. More notable is the lack of any evidence whatsoever — in this report or any other that we’ve gotten recently — to suggest the market is correct to price in 100 basis points of Fed rate cuts by January. That gap between market pricing and (likely) reality, which I wrote about in depth last week, remains a live risk despite the relatively good news on consumer prices this week.

What is an investor to do?

Even if banks don’t self-regulate themselves into a credit crunch, the U.S. doesn’t default us into a recessionary financial crisis and rents continue to drag down inflation, investors still face an uncertain road ahead. And they seem to know it! Institutions are on their back foot:

And individual investors are bearish on stocks:

Bill Gross made news this week by suggesting investors buy Treasury bills, which he rightly pointed out are yielding more than any similarly-rated fixed income security at the moment. He has a point. There is no chance investors will experience a permanent loss on their Treasury bills, even in the event of a technical default next month. At worst, this would entail a delay of a day or two while the world caves in on itself and the debt ceiling is quickly raised by panicking lawmakers.

The last time the debt ceiling became a significant source of market concern, S&P downgraded the U.S. credit rating as punishment for the brinksmanship. It came as a surprise to some that Treasuries and the U.S. dollar rallied on this move while risk assets sold off. There is every reason to think something similar would happen this time as investors flock to safety in times of uncertainty. Long-duration, high-quality bonds would also come in handy in the event of the severe credit crunch and recession in bear scenario #1, although they would clearly struggle with bear scenario #3, the higher-for-longer inflation scenario. Treasury bills and cash would perform fine in bear scenarios #1 and #2 and, based on recent experience, would likely be the leading asset class in bear scenario #3. So, whatever you’re worried about, cash and bonds across the maturity spectrum clearly have a place in portfolios right now.

But what about the benign base case? Well, there’s good news and bad news. First, the good news: Market losses are unlikely if the economy slogs through this period and lands softly, and asset class correlations have already begun to return to their pre-2020 normal, implying lower volatility for diversified portfolios:

The bad news? With rates slow to come down, bond prices won’t budge and equity valuations will be hard-pressed to move up. Investors are going to need to crawl out of this with high current yields and rising estimates of future earnings supplying the growth.

What to watch for over the next week (and beyond)

We’ll get evidence on two areas of the U.S. economy that seem to be cycling up (industrial production and home construction) and another that seems to be slowing (retail sales).

April data out of China is expected to show a large acceleration in activity across the major segments of the economy. This week, export data showed faster-than-expected growth while imports disappointed. Hmm…

What else I learned last week

I learned that’s it’s regrettably too late to get my wife a scorpion in lucite for Mother’s Day (from the kids!) Perhaps I can stage a romantic balcony scene that falls somewhere between Romeo and Juliet and Tom and Shiv.1

I learned that dance recital season involves an endless loop of carpooling, not to mention money for costumes, tickets, videos and memorabilia flowing out of my bank account like water through a sieve.

I learned that my 5-year-old’s Cub Scout den, when given the choice between “Building up” or “Knocking down” a stack of paper cups, made the incorrect but predictable choice. What did this remind me of? Oh, yeah!

I learned that my 7-year old managed to recreate a 32-team soccer tournament bracket complete with club and country crests from memory on a poster and I think maybe I need to take the FIFA 23 game away for a few days.

I learned that I’m finally having a “guys’ night” tonight with some other dads in my town, which only happened because we told our wives they had to arrange it for us. And they came through, like they always do!

{kind=link}

Cheers,

Brian

For those of you who are confused, those are Succession references.