Let's just see how this goes, shall we?

Say good-bye to rate hikes and hello to a (hopefully) long pause

“This is the end. Hold your breath and count to ten.” - Skyfall, Adele

May 5, 2023 - Bottom line up top

Anyone looking for signs of a recession shouldn’t bother to look at the April U.S. employment report, which showed rising employment and faster wage gains.

The Fed hiked rates, probably for the last time this cycle as it anticipates tighter credit conditions to weigh further on growth and inflation. But the rate cuts priced in for this summer won’t happen unless the labor market weakens.

JPMorgan’s acquisition of First Republic Bank was more orderly than the previous unwinds back in March. While we may see more consolidation, the main economic threat is restricted credit access for consumers and businesses.

Absent a genuine credit crisis or debt ceiling coup de grace, the U.S. economy shows very few signs of tipping into recession. Home prices and car sales are up, real incomes are rising, and hiring remains strong.

Stocks are bending but not breaking on the bad bank news, likely because first quarter earnings have generally come in less negative than expected. But a large leg up for stocks from here is still hard to imagine in the near term.

Long-term interest rates have peaked, while credit spreads have impressively resisted both the banking scare and the expectation for slower economic growth. Yields on various types of credit remain attractive compared to equities.

Chart of the Week

U.S. auto sales surged again in April after a strong Q1, a sign consumers are still alive

Call off the recession! The April jobs report still shows a hot economy

The doom and gloom society will have to wait at least another month for evidence the U.S. economy has tipped into recession. The April U.S. employment report shows the labor market started out hot in Q2 after cooling more than we previously thought at the end of the first quarter.

Non-farm payrolls increased by 253,000 last month, far more than expected and the most since January as gains for both February and March were revised down substantially. Employment also increased in the household survey, bringing the U-3 unemployment rate back down to a decades-low 3.4% and the prime age employment rate up to 80.8%, the highest it’s been since 2001. The post-pandemic “lazy worker” hypothesis is well and truly dead.

Risk assets may greet the blowout jobs report as bad news, because it reintroduces the risk of further Fed hikes (more on the Fed in the next section). Indeed, average hourly earnings — a poor proxy for wages because of their composition effects, but closely watched nonetheless as a guide to future inflation — rose by more than expected. Longtime readers know I’m always a “good news is good news” type of guy following reports like this one. An economy that’s creating jobs and seeing real wage increases for workers is not one that looks likely fall into recession even with interest rates at elevated levels. And recession is what we want to avoid the most.

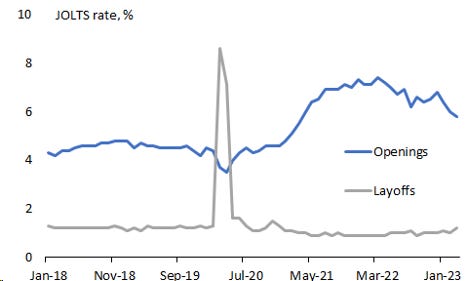

So, this morning’s report was a little too warm to be called Goldilocks. But Tuesday’s JOLTS data showed the labor market is normalizing in exactly the way we want. Of course, this sent investors into a panic. [Deep breath] Layoffs are now about as common as they were in 2019, while quits (i.e., voluntary separations) remain uncommonly high even after their recent decline. Job openings have come down but still outnumber unemployed workers by more than 1.5 to 1. (Alas, writing free weekly newsletters does not constitute employment. I’ve looked into this).

Job openings are down (but still high) and layoffs are up (but still low)

As Fed Chair Powell himself admitted this week, economic models tell you that the job vacancy rate should not be able to fall from 7.4% to 5.8% without an increase in unemployment. There’s no such thing as a free lunch (except my Mom’s delicious pea soup, which I’m eating as I write this). So either a) the apparent rise and fall in job vacancies over the past two years wasn’t real; or b) the U.S. economy suffered an unprecedented trauma in recent years that warped traditional economic relationships in a significant but ultimately temporary way. While I think it’s a little of both, as the economic effects of the pandemic recede, things are returning to the 2019 “normal”.

Just so I don’t come across as too Pollyannaish, I’ll admit it’s still not clear whether we are on a smooth descent to normal or merely passing through normal on our way to, well, something bad. A recent turnaround in housing data and evidence that inventories are being rebuilt in Q2 suggests a soft landing is still very much in the cards (it remains my base case). And as the featured chart above shows, consumers continue to make big purchases in sectors like autos where supply constraints remain an issue, even if those purchases need to be financed at relatively high interest rates. And this morning’s employment data showed no signs that initial concerns about financial stability and slowing growth in March led to a noticeable decline in hiring. It’s harder to make the case the U.S. economy is anywhere close to recession after this week’s data.

Good-bye and good riddance to Fed hikes…but don’t expect cuts yet

The U.S. economy grew at a paltry 1.1% rate in the first quarter.1 S&P 500 companies’ earnings are down compared to last year. The FDIC just had to midwife the sale of one of the country’s largest banks as it stumbled toward failure. And the U.S. Treasury is mere weeks from a potential default. Despite all of this, the Federal Reserve raised its policy benchmark rate this week above 5% for the first time since the mid-2000s in an effort to further slow the U.S. economy. Perhaps the most surprising thing about it was that no one was surprised.

Simply put, inflation has not been coming down as quickly as the FOMC desired, and that means rates needed to go higher. Just to prove how serious it is, the Fed hiked through a housing recession, a manufacturing stall and a banking scare — all of which the hikes helped bring about! The mystery for me has always been how exactly the Fed thought hiking rates so much and so quickly would bring down this particular vintage of inflation, which has been driven more by profit margins than labor costs. The plan simply seemed to be to hike until something broke, and now that California’s banks are breaking, the Fed feels it can stop. This week’s statement had the air of finality to it, as the committee believes the new 5.00% - 5.25% target range will represent a plateau for this cycle.

Here’s the thing, though. Markets aren’t pricing in a plateau. They’re pricing in a sharp peak, with rate cuts arriving by September and continuing throughout 2024. Folks, if the Fed is cutting rates this summer, something has gone horribly awry and investors will be suffering. But even if the market is wrong about the cuts, its current disconnect with policymakers still poses risks. For more than a year, the main source of financial market volatility has been the gap between where investors expected the peak federal funds rate to top out and where it has actually ended up. Now that everyone seems to agree that rates hikes are over, the misalignment has shifted to the timing and magnitude of rate cuts.

This week, the gentlemen's disagreement between the market and the Fed on where rates will be at the end of 2024 widened to almost 150 basis points. As we found out last year, gaps of this size are rarely conducive to market tranquility.2

Markets are pricing in more than twice as much easing next year as the Fed expects

Even Fed nerds like me will be happy to see Chair Powell and his merry crew recede into the background as their meetings become less consequential for markets. Monetary policy has clearly become more of a dependent than an independent variable, hostage to the data. What will replace the Fed in the headlines, however, remains an open question. Let me spell out in a bit more detail what I’m watching in the coming weeks for guidance on investment strategy.

What to watch for over the next week (and beyond)

Fed hikes could continue if core inflation fails to normalize further. in the context of a strong economy. Next week’s April consumer price inflation data may show the lagged effects of declining new rent growth starting to bring down average rent inflation. Prices on other services may be slower to moderate even as wage growth slowly declines.

Next week, I’ll write about the debt ceiling showdown, which has the potential to become a default crisis next month unless sanity prevails. Money markets are noticing, as are Treasury bill traders. It won’t be long before equity and credit markets feel it, if they haven’t already. But the most likely scenario given the lateness of the hour is for a clean but short debt ceiling extension into the fall to align with budget negotiations, which are just now beginning.

The Bank of England will raise rates by 25 basis points, in line with the Fed and the ECB decisions this week. Governor Bailey and his colleagues will likely hike a few more times this summer with core inflation proving hard to tackle.

What else I learned last week

I learned that it’s a good idea to bring a change of clothes for your kids to any party that involves both an inflatable bounce house and four hours of pouring rain. (But then try explaining to the 5-year old that once he has the dry clothes on, there’s no more going on wet bounce house!)

I learned that following up our bedtime reading selection of Moby Dick with 20,000 Leagues Under the Sea (both abridged versions for kids…I’m not insane) has stirred a discussion of who the better captain is, Nemo or Ahab. This isn’t even close, obviously. It’s Nemo.

I’m a few years late to this, but I learned that The Nun (HBO Max) is really terrifying, and I don’t think my 10-year old daughter should have let me watch it.

I learned that I was pretty concerned when the 7-year old told me five minutes before the start of his First Communion mass that he was going to throw up. (He didn’t. Crisis averted.)

I learned that someone needs to hire Bryan Cox away from those DirectTV commercials and pay him to do “doctored” Dead Logan Roy gag reels in front of a green screen. Kind of like a morbid version of Cameo. Unbelievable growth.

One note before I close. I’m overwhelmed by the number of new subscriptions this week after I announced I was starting this newsletter. Thank you all so much for signing up and reading. And thank you especially to those who offered to become paid subscribers! You might notice you still have your money. That’s because I don’t have paid subscriptions turned on at this time, mainly because I’m not sure how long I’ll be doing this and don’t want to accept money for a year’s worth of newsletters that I may never write. But if anything changes, you’ll be the first to know…because I’ll have your money.

Thank you all, again!

Cheers,

Brian

It was actually quite a bit better than the 1.1% rate suggests, as I covered in my final non-Substack newsletter least week, but headlines are headlines.

One caveat here lest I sound too negative: the FOMC dot plot shows the median forecast from a group of roughly 20 people, while the fed funds futures market shows more of a probability-weighted mean for an entire market. If 20% of fed funds futures traders think the economy is headed for an iceberg and rates are going back to zero, their influence can bend down the curve even if the median trader’s base case looks more like the Fed’s. Even so, the process of shrinking this gap, whether it comes from capitulation from the Fed in the face of recession or investors accepting that rates are going to stay higher for longer, may result in some pain for markets.

Congratulations on that first communion from a Former Colleague who got the discriminatory COVID axe after request for medical and religious exemption were denied. God's will be done. Glad to get your missives - I genuinely missed your Friday morning emails and I look forward to learning about the next stop for you.

Superb writing, Brian. What a great read this morning, with just enough personality to make the news cycle manageable. That mismatch of market expectations vs Fed vision is a hot area of research.