Unlearning the investing lessons of 2022

Plus: A deep dive into the just-released May U.S. jobs data

Lt. Aldo Raine: Y'know, Utivich 'n myself heard that deal you made with the brass. End the war tonight? I'd make that deal. How 'bout you Utivich, you make that deal?

Pfc. Smithson Utivich: I'd make that deal.

Lt. Aldo Raine: I don't blame ya! Damn good deal!

Inglourious Basterds, 2009

June 2, 2023 - Bottom line up top

The debt ceiling drama is over and U.S. economic data has been strong, so we’ve all decided that the next big risk is whether the Fed has to keep hiking rates to get inflation down. How quickly things change…and change back.

Payroll growth remains shockingly strong, and hourly earnings continue to show signs of easing. A resilient labor market tends to create resilient consumers.

Your weekly bit of good news on the U.S. housing market: Home prices rose again in March and the cumulative decline in most places in the country was quite small. This may be why we’re seeing building pick up this spring.

“Soft” data out of China this week provided no clarity about the strength of the manufacturing recovery there. Two PMI surveys pointed in completely opposite directions. We can surmise from the behavior of China’s equity market and its monthly hard data releases that the reopening has been weak.

While leaks to the Wall Street Journal have persuaded investors the Fed won’t hike this month, market pricing still shows a 70% chance of a hike in July. While this won’t break the economy, the Fed’s updated economic projections will be closely watched. Only two weeks away!

Following a swift recovery from the banking scare, a run of good earnings, and positive feelings toward tech, stocks are being challenged once again by the macro environment, with hawkish policy and slowing growth are the expectation.

Stock-bond correlations have reverted to their negative pre-2022 norm. Diversification should not be considered a dirty word for investors positioning for the balance of the 2020s.

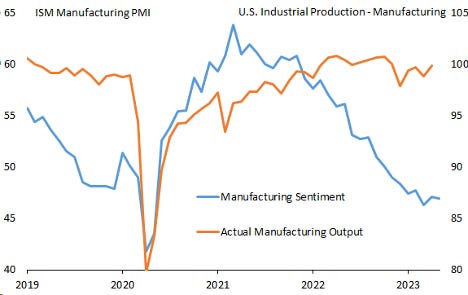

Chart of the Week - Stop paying attention to PMI polls!

Manufacturing sentiment is in the dumps, but actual manufacturing activity is on the rise

Mostly good news in a messy May U.S. employment report

The May U.S. employment report was a good example of what can happen when you have two different surveys being reported simultaneously. The establishment survey, which covers businesses, reported explosive payroll growth of 339,000, blowing away the median forecast of just under 200,000. In addition, payrolls for previous months were revised up by nearly 100,000. Construction employment, in particular, is booming, consistent with the single-family housing starts bounce we’ve been seeing.

That’s the good news. The bad news is that the household survey, which canvases individuals, reported a decline in employment of 310,000 and an increase in unemployment of 440,000. This caused the unemployment rate to rise to 3.7% from 3.4%, a large jump for a single month.

Now, there’s a reason you tend to see the establishment survey quoted more often when it comes to job creation. It exhibits less volatility month to month and tends to tell a more accurate picture of what’s happening in the labor market. While we shouldn’t dismiss the household survey swoon out of hand, we’ve seen blips like this before only to see them offset a month or two later. The actual pattern of job creation over the past eighteen months certainly looks a lot more like the orange bars than the blue ones:

The rest of the report pretty much delivered on expectations. Prime-age labor force participation remains at its recent high while average hourly earnings growth decelerated. Despite the very strong payroll growth number, there’s nothing in this morning’s survey that is likely to cause the leadership at the Fed to feel the need to raise rates at the June meeting.

When the most prominent monthly report delivers mixed signals, it’s good to look at the rest of the data landscape for corroborating evidence. But on Wednesday, the Job Openings and Labor Turnover Survey (JOLTS) showed what it usually shows: It’s really hard to report consistent and usable monthly survey results with a very low response rate! Taken at face value, the report showed that after three straight months of gently declining job openings, employers posted over a quarter million net new positions in April, bringing total openings back above 10 million. Treasury yields flailed about on the news, but let’s not get hysterical. The JOLTS report is noisier than most monthly releases, but it’s telling a consistently benign story when you zoom out:

Fewer people are quitting work voluntarily, and job openings, while down significantly from their March 2022 peak, remain elevated. But layoffs are still rare. This continues to look like a labor market in the process of normalizing, not cratering.

Job report Fridays provide an opportunity to take a deeper dive into an ongoing trend in the U.S. labor market. I mentioned earlier that the U.S. employment rate has recently risen to its highest level in decades as a result of strong demand for labor and an unexpectedly deep supply of workers. Many of these “extra” workers are teens electing to work instead of enrolling in 2-year colleges:

The trend in 2-year college enrollment maps closely (and inversely) onto this graph of employment among 16-19 year olds, which bottomed in the early 2010s as 2-year college attendance peaked:

The U.S. labor market remains remarkably strong. Unemployment claims are low, monthly job creation is robust and wage growth, while elevated, is starting to come down. A few weeks ago, I wrote about the U.S. economy returning to something that looked like late-2019 or the first few months of 2020 as a good definition of a soft landing. The labor market is pretty much there.

Investors must unlearn the lessons of 2022

In the moment, 2022 felt like the start of something new for investors. Asset class correlations reversed (to positive territory) at the worst possible time. Interest rates rose higher and faster than they had in recent memory amid surging inflation and rapid policy tightening. And the tried and true 2010s investment strategy of a) holding the S&P 500 index; with b) a concentrated position in mega-cap of tech or tech-adjacent companies failed miserably. A lot of portfolios managers — and more than a few talking heads — told us all we needed to embrace a new investing paradigm. What, precisely, that was supposed to be was never quite clear, but it probably had something to do with whatever “strategy” they were selling.

Well, we’re now almost halfway into 2023 and the best investment strategies have been…owning the index, carving out a position in U.S. mega cap tech, and improving risk-return efficiency through diversification. Whatever you think 2022 taught you…well…

Of course, some of the effects of 2022 are still with us. Interest rates haven’t declined, which, as I showed last week, should allow bonds to provide more competition for stocks in the coming years than they did throughout most of the 2010s. But even if stocks beat bonds for the remainder of the decade (and they probably will) investors should be happy that asset class correlations are returning to normal:

Answering the question, “what portfolio should investors hold for the balance of the 2020s?” is complicated. But step one is a commitment (or a recommitment) to diversification, despite what occurred last year. This means that virtually all investors should at least hold a mix of stocks and bonds in their portfolios. Investors with higher net worths and fewer liquidity concerns can consider additional asset classes, which I’ll discuss in the weeks ahead.

What to watch for over the next week (and beyond)

The Fed doesn’t meet until the 14th and won’t get any more comments from FOMC members between now and then. I don’t expect a hike, but there’s a very good chance that the “dot plot” shows rates going higher before the end of the year and declining only slightly in 2024. A hawkish outcome is possible even if they skip a rate hike.

China’s trade data has been all over the place lately, but it’s clear that weaker global demand for goods is hurting manufacturing and exports while the services-centric reopening has been weaker than expected. This is one reason we’ve seen global commodity prices dropping and news this morning that China is considering options to bolster its flagging property sector.

U.S. household balance sheets have been supporting the expansion. Next week, we’ll get consumer credit data for April, which will likely show continued strong borrowing growth, and a household balance sheet snapshot as of the end of Q1. Net worth almost certainly increased in Q1 on stable home prices and surging financial asset values.

What else I learned last week

I learned that my 8-year old wants to set up a lemonade stand to raise money to buy Sisu (a movie best described as an ultra-violent Finnish — yes, Finnish — John Wick) on streaming. It’s great that he thinks lack of funds is the binding constraint here.

I learned that the Succession (Max) finale ended as it should have with the beleaguered hero, on top. I wish he had told Shiv that she must know — surely she must know — it was all for her.1

I learned that the Barry (Max) finale was tense, wicked, darkly funny and rewarding for those who binged the first three seasons (while I had Covid!) but had to wait patiently for the fourth.

I learned that back-to-back dance recitals for the 10-year old bisected by an outdoor picnic with 35 minutes of driving each way is a perfect way to spend the Sunday of Memorial Day weekend. Only eight more years of these left!

I learned that my 8-year old managed to get injured while marching with his Cub Scout pack in the Memorial Day parade. A patriotic fellow scout poked him in the eye with a miniature American flag. Fortunately, he made a full recovery.

I learned that I’m chaperoning a field trip for my 5-year old in 35 minutes…and it’s 30 minutes away. Gotta go!

Cheers,

Brian

Deep cut there for P&P fans.