Wake me up when we get to 2019

Plus: Don't pay attention to what consumers say. Pay attention to what they do.

But all you wanted was tomorrow

And box your yesterdays away

You forgot your time was borrowed

And it's just another day

“All You Wanted Was Tomorrow”, Dave Matthews Band, 2023 (New Album Out Today!)

May 19, 2023 - Bottom line up top

U.S. recession risks receded further this week as core retail sales and industrial production data for April both came in stronger than expected. Continuing jobless claims are falling, and it looks like the debt ceiling will be raised.

Housing and manufacturing had recessions in 2022 but are now in recovery mode, providing a cushion as consumer spending moderates. Rising single-family building permits corroborate the surge in homebuilder confidence.

Stocks are pricing in an economic soft landing while credit remains jittery because of the debt ceiling and banking concerns. Interest rate futures no longer show the rapid Fed easing that would be consistent with a recession.

Corporate earnings estimates appear to have bottomed, and year-on-year profits growth should resume by Q3 as long as the guidance we’re getting from companies holds up (it should…see the first bullet).

Fixed income markets are next to impossible to untangle while the debt ceiling still looms. While the 1-month bill offers an attractive rate of return, longer-maturity debt will provide a better hedge against worst case macro outcomes.

Chart of the Week: Early cycle (again) for the U.S. housing market

After last year’s housing recession, single-family starts and permits are increasing

Consumers don't believe their own surveys. Neither should you.

The past few years have often featured a wide divergence between so-called “hard” and “soft” U.S. economic reports. Nearly all data is collected using a sampling method (the BLS doesn’t calculate the unemployment rate by interviewing every American every month asking if they have a job), but hard data like consumer spending and industrial production represent real world economic activity. Soft data, on the other hand, refers to sentiment surveys, also known as opinion polls.

In order to make them look more like hard data, these poll results get shoehorned into a quantitative format like a diffusion index. This gives you very precise-seeming results like “the ISM Manufacturing PMI rose last month to 47.1 from 46.3.” And we’re all supposed to “ooh” and “aah” and hold our chins at interesting angles. But the questions in the survey are binary, e.g., whether delivery delays are better or worse than they were the previous month. One of the things they teach you in sixth grade math is that your output can only be as precise as your input. The same principle applies here, but that doesn’t stop slight changes in soft data from getting undue attention from markets.

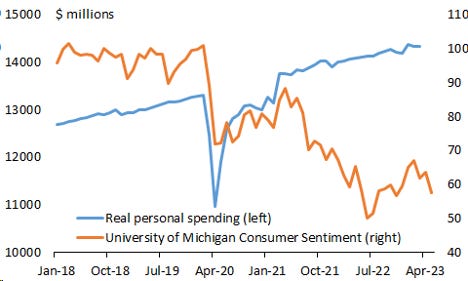

Sentiment can fluctuate for any number of reasons, response rates, which have been lower since 2020. Inconsistent replies make surveys less useful gauges of what’s happening in the real economy. But you don’t have to take my word for it. Take a look at this graph, a classic of the genre, of real consumer spending vs. University of Michigan Consumer Sentiment:

{kind=link}

The other thing going on here, of course, is bias. Surveys are filled out by people, and people have biases. Right now, a lot of people are telling survey takers things are terrible both for them personally and the country as a whole, but they’re behaving as if everything is perfectly fine. “Yes, we’re taking two vacations this summer and going out to eat every week. But the economy is terrible!” Small businesses hiring plans peaked in August 2021, but monthly job creation has stronger than expected just about every month since then. Some response biases are political. Republicans currently report the U.S. economy as worse than it’s ever been (2008? 2020?!) while Democrats say it’s about the same as it was just before the pandemic. I’ll have more to say about this in the next section.

Investors should ignore the vast majority of survey data. But they don’t. A lot of strategists use the ISM Manufacturing Purchasing Manager Index, for example, as an indicator for the equity market or the U.S. economy. Detecting inflection points in economic cycles is important for both bottom-up and top-down investment strategies, so it’s no surprise that cyclical indicators are popular divining rods (I’ve been reading a novel about water dowsing to my 5-year old — unsurprisingly, it makes him fall asleep — so this metaphor was front of mind). But today less than 20% of the U.S. economy is manufacturing, making the ISM a less reliable fortune teller for our collective fate.

What should we look at? My checklist for whether things are good/bad and likely to get better/worse (because, after all, current economic activity is the best predictor of future economic activity) is:

The consumer spending/employment rate link. More people working means more people spending means more people working. Weekly jobless claims plus real consumer spending and disposable income are at the top of this list.

Manufacturing activity (e.g., industrial production) and inventory levels (which are often a leading indicator for future production).

Private construction and public infrastructure spending.

Growth in personal credit balances vs. overall household net worth.

This list is far from comprehensive, and not everyone on it is shining a bright green light at the moment (though I think the only “yellows” are commercial and multi-family real estate construction and consumer credit growth). But the words “confidence” and “sentiment” do not appear on it. Look at what people and companies do, not at what they say.

The economy is headed into the future. All the way…to the year 2019.

Back in my college days, Late Night with Conan O’Brien was nightly appointment viewing, which tells you something about my sleeping habits at the time. Perhaps his most famous bit — other than a certain bear whose unshakeable habit I can’t adequately describe in this family-friendly newsletter — was looking into the future. Far into the future. All the way…to the year 2000. This gag began in the late 1990s but continued in the year 2000 itself and then well past it, which made it even funnier. While my clairvoyance is not strong enough to see all the way to the year 2000, I can just make out the U.S. economy nearing another milestone: the year 2019.

Ah, 2019! Before Zoom calls. Before direct-to-streaming blockbusters. Before low unemployment and high prime-age labor force participation. Hey, wait! We actually did have those last few things in 2019:

And 2019’s positive economic vibes weren’t limited to the labor market. By the end of that year, we’d mostly shaken off the effects of the trade war with China, which had helped trigger a shallow earnings recession even as GDP growth remained steady. Manufacturing activity picking up with demand strong and inventories close to a bottom. Real income growth was healthy, but there was no threat of a wage-price spiral. U.S. consumers had the economy on their backs, but home construction was also surging after a swoon in the first half of the year. Investors didn’t expect imminent action from the Fed on rates in either direction, but there was a good chance of cuts priced in over a 6-9 month horizon.

Does any of this seem familiar? Jay Powell has often spoken about his informal goal of restoring the 2019 economy, when he had the plane in the air at a safe altitude and no one was asking him how or when he was planning to land it. The path to an economic soft landing from here ends at something that looks a lot like the economy as it was at the end of 2019.

Of course, there are many important differences — good and bad — between 2023 and 2019! Excess household savings are significantly higher today. The flow of immigrants with work visas is strengthening instead of weakening as it was in 2019. Government infrastructure spending is set to kick into a higher gear soon. On the other hand, personal savings rates are lower, interest rates are higher and inflation is starting from an elevated rate instead of a subdued one. This is why even as most parts of the U.S. economy are either stable or improving, we can’t yet say that a soft landing is assured. Disinflation, stable employment, and a benign fall in interest rates are the benchmarks for success over the next few quarters. So far, so good.

What to watch for over the next week (and beyond)

The main event will be the April personal income and spending report, which over most of the past year has shown incomes growing in excess of inflation and solid though slowing real spending growth. I’m expecting more of the same.

This week’s surprisingly hawkish commentary from FOMC voters will focus more attention on next week’s release of the May meeting minutes. The lack of obvious spillover from the banking scare into the wider economy as well as the apparent debt ceiling resolution will allow the Fed to focus more on inflation, which means another Fed hike in June is likelier now than it was on May 3rd.

We’re going to get lots of soft data via preliminary global PMIs for May. You can safely ignore it, even if it confirms your priors. Especially if it confirms your priors!

New home sales have been on fire with existing homeowners sitting on their 2.75% mortgages and providing little new inventory for sale. We’ll get April data next week. Weekly mortgage applications have been steady, as have rates. I’m not expecting much change to the trend.

What else I learned last week

I’m still listening to the last few songs as I write this, but I learned that Walk Around the Moon is the best Dave Matthews Band album in twenty years. It gives me great pleasure to report this. See you at Jones Beach this summer, Dave.

I learned that approaching dance recital season is like flying up to a black hole. Time and space are no longer behaving according to the established rules of physics as everything — time, gas, family members and, of course, money — is pulled toward a single fixed point.

I learned that if I ran a T.V. show and wanted to give about 85% of my audience acute anxiety and PTSD, I would write the election episode of Succession that aired last Sunday.

I learned that the Giants somehow don’t have a daytime home game until late October, but the newly-minted 8-year-old is psyched for his first ever game to be against Zach Wilson and the winless Jets.1

I learned that the 8-year old also showed an almost frightening understanding of what was going on in The Matrix in his first viewing2. We need to disabuse him of his dream of becoming a professional athlete and get him involved in AI research. As a diligent law enforcement officer once said…

{kind=link}

Cheers,

Brian

Yes, this is me trolling Jets fans. One of my favorite pastimes. I know you have Aaron Rodgers, but I just think Zach beats him for the job in camp. (Again, trolling…maybe)

Why am I showing my 8-year old The Matrix? First, I’m just not a good Dad when it comes to age-appropriate movie viewing. Second, he literally asked me “what if nothing is real?” How often is there a sci-fi classic ready made to answer your child’s existential questions?

Thanks for the update, Brian. Your dance recital observation also rings true - for some reason, they can never re-use their costumes either, but its heresy to ask why.

Great article, Brian.